Property is a good investment in India only in the forms that actually pay you: residential rental yields just 2-3.5%, commercial 6-9%, REITs pay variable market-linked returns, while a branded resort sale-leaseback pays a contractual 8-10% on a registered, owned asset. A second home that sits empty is a store of value, not an investment.

Ask most Indians whether property is a good investment and the answer is instinctive: yes. But dig a little and you find that what they own is usually a second home or a plot — an asset that appreciates slowly, sits empty for much of the year, and quietly costs money in EMIs, maintenance, and property tax. That is property as a store of value, not property as an investment.

Treated as a genuine investment, real estate should do one thing above all: pay you a real, recurring income — on top of any appreciation. This guide breaks down the four practical ways to hold property as an investment in India, what each one actually yields, the "second-home trap," and why, for income-focused investors, a branded resort unit increasingly wins.

What makes property a good investment?

Stripped of emotion, real estate earns its place in a portfolio for four reasons:

Income. Rent (or rental-equivalent) that arrives whether or not the market is up.

Appreciation. The asset value rising over time.

Inflation hedge. Property and rents tend to rise with inflation, protecting purchasing power.

A real, owned asset. Unlike a fixed deposit or a bond, you hold something tangible, financeable, and transferable.

The catch: most of these only show up if the property is working. An empty second home delivers appreciation and an inflation hedge — but no income, while still charging you for the privilege. The investment-grade versions of property are the ones that pay.

What are the ways to hold property as an investment in India?

1. Residential rental. Buy a flat, rent it out. Familiar and liquid-ish, but Indian metro rental yields are low — typically 2–3.5% — and you carry tenant management, vacancy gaps, and upkeep.

2. Commercial property. Shops or offices yield more (6–9%) but need larger capital, carry tenant-concentration risk, and are harder to exit.

3. REITs / SM REITs. Buy units in a listed real-estate trust. Liquid, diversified, professionally managed — but you own a paper unit, not a specific asset, and returns are market-linked and variable. (More in our fractional ownership guide.)

4. Branded resort sale-leaseback. Buy a registered unit inside a branded resort; a hotel operator runs it and pays you a contractual 8–10% annual rent, plus owner stay-nights. You own a real, deeded asset and earn hospitality-grade income without managing anything. See exactly how it works →

Each is right for someone. But if your goal is high, predictable income from a real asset you actually own, options 1–3 each give up something on that exact axis — and option 4 is built around it.

What each one actually pays

| Option | Typical Yield | Own a Real Asset? | Who Manages It | Liquidity |

|---|---|---|---|---|

| Bank FD (for reference) | ~7% | No | — | High |

| Residential rental | 2–3.5% | Yes | You | Medium |

| Commercial property | 6–9% | Yes | You / agent | Low |

| REIT / SM REIT | Variable | Units only | Trust | High |

| Branded resort (leaseback) | 8–10% contractual | Yes | Operator | Low–Medium |

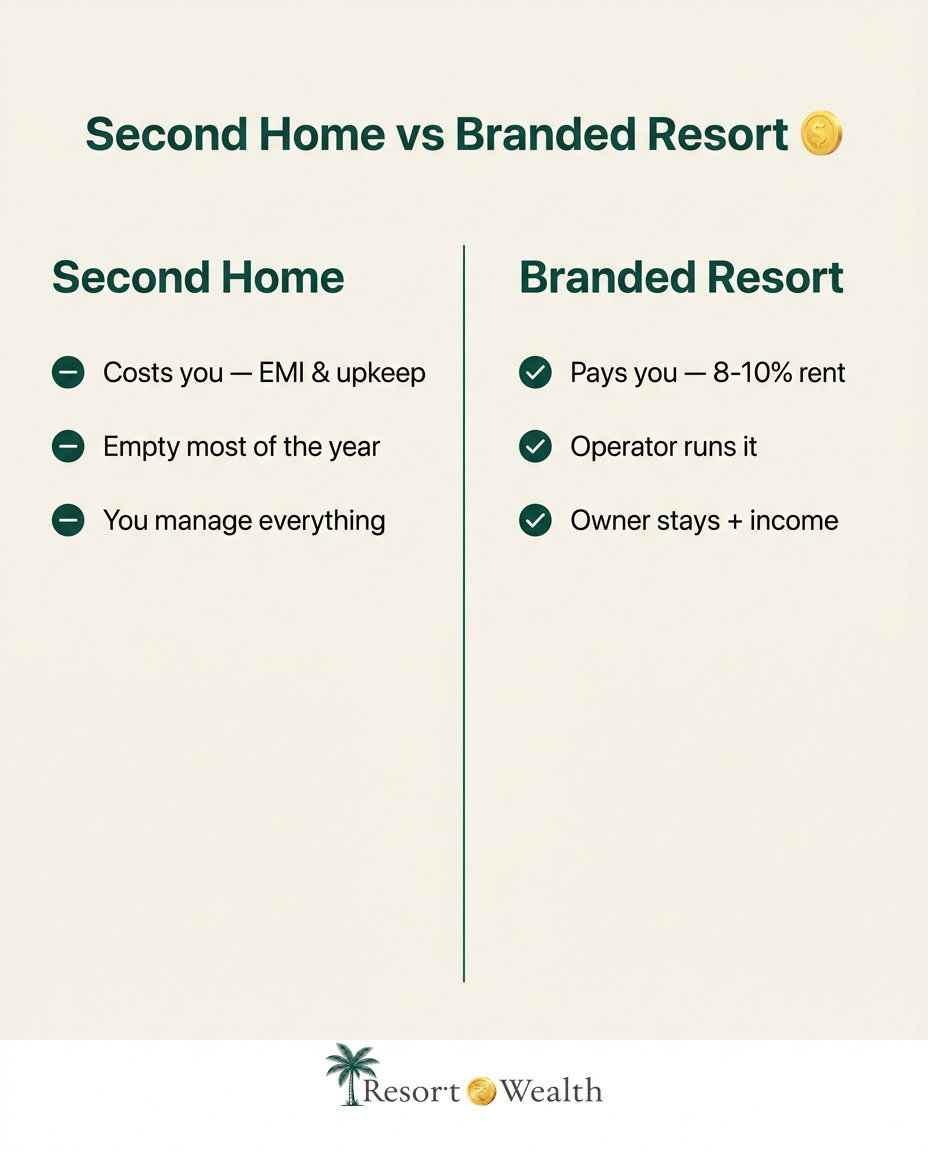

Is buying a second home a good investment?

A second home is the most common "property investment" in India — and often the weakest one financially. Here is the honest math: you tie up ₹1–3 crore, use it a few weeks a year, and pay EMIs, society charges, property tax, and upkeep for all twelve months. Appreciation may eventually reward you, but year to year the asset is a net cash outflow.

A branded resort unit flips that equation without giving up the lifestyle. You still get the holiday — owner stay-nights at a 5-star property — but the operator fills the unit the rest of the year and pays you a fixed rent. Same emotional benefit; opposite cash flow.

How much does ₹50 lakh in property actually pay?

Put ₹50 lakh to work and the income gap is stark:

Bank FD at 7%: ₹3.5 lakh a year — fully taxed, no asset, fully liquid.

Residential rental at 3%: about ₹1.5 lakh a year — plus tenant hassle and vacancy risk.

Branded resort at 9%: ₹4.5 lakh a year — contractual, paid quarterly, a registered asset in your name, plus owner stay-nights.

The trade-off you accept for that higher resort yield is honest and real: illiquidity (plan a 5+ year hold) and operator dependence (the rent is only as strong as the operator paying it). For income-focused investors who can hold, that trade is often worth making — but only after the project, lease, and operator are verified.

Who should treat property this way — and who should not

Good fit: you want fixed, real-asset income; you can lock capital for 7–10 years; and you would value occasional luxury stays. NRIs fit especially well — a registered Indian asset earning contractual income, with FEMA-compliant repatriation.

Poor fit: you need the money back within 2 years, this would be your only asset, or liquidity matters more than yield. In those cases an FD or a REIT is the more honest answer — and a good advisor will tell you so.

"Good" and "good for you" are different sentences. Property is a genuinely strong investment — but only in the form that matches your goal.

Bottom line

Property is a good investment in India — but mostly in the versions that actually pay you. A second home stores value while charging you to hold it; a working asset earns. Among the income-focused options, a registered branded resort sale-leaseback stands out for combining a real, owned asset with a contractual 8–10% yield and lifestyle use — provided you verify the structure.

The right next step is not "buy property." It is "match the right form of property to your goal." That is the question worth answering before you commit a rupee.

Frequently asked

Ready to invest?

Free advisor consultation — get a personalised investment report with current property availability, RERA documents, and unit-level projections.

💬 Free Consultation